In today’s financial ecosystem, bank loans play a crucial role in helping individuals and businesses achieve their goals — whether it is buying a home, starting a business, funding education, or meeting personal needs.

However, many loan applications get rejected every day. What surprises most borrowers is that loan rejection is not always about a low credit score. Banks evaluate several aspects of a borrower’s financial profile before approving a loan.

Understanding these factors can significantly improve your chances of getting a loan approved.

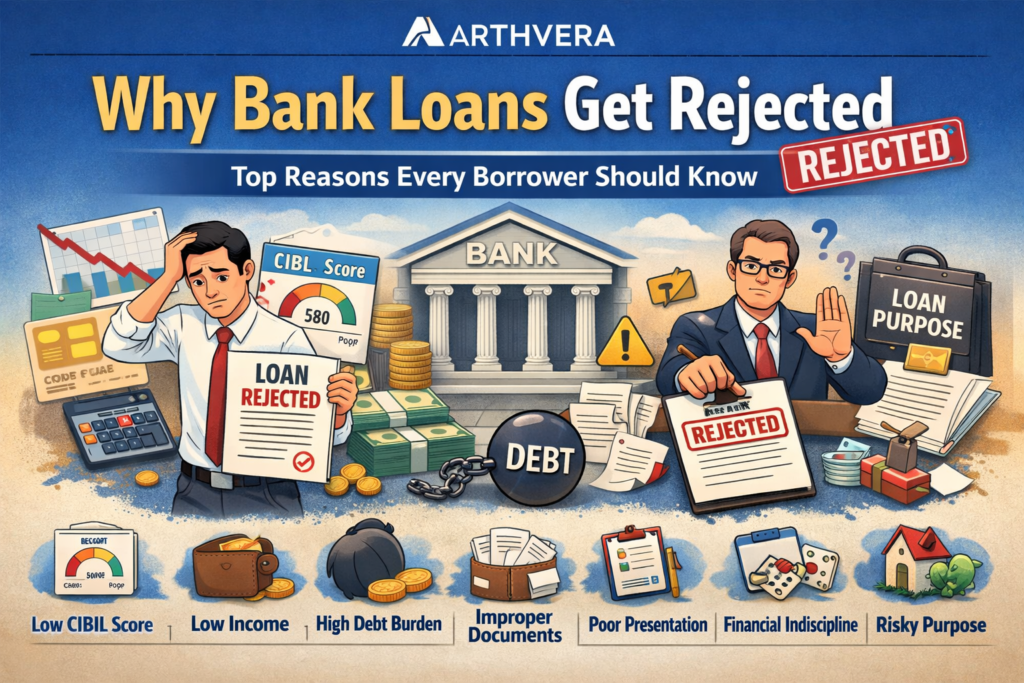

Let us look at the seven most common reasons why bank loans get rejected.

1. Low CIBIL Score

Your credit score is one of the first things banks check while processing a loan application.

A CIBIL score below 700 generally signals higher risk to lenders. It indicates past repayment issues such as delayed EMIs, defaults, or high credit utilization.

A strong credit score reflects financial responsibility and significantly increases the chances of loan approval.

2. Insufficient Income

Banks carefully evaluate whether your income is sufficient to handle the proposed loan EMI.

Even if your credit score is good, a loan may still be rejected if the bank feels that your income is not adequate to sustain the repayment burden.

Lenders assess income stability, employment type, and salary consistency before approving the loan.

3. High Existing Debt Burden

Banks also examine your Debt-to-Income (DTI) ratio, which measures how much of your income is already committed to existing loans.

If a large portion of your income is already used for EMIs, the bank may consider you financially stretched and reject the loan application.

A healthy financial profile generally keeps total EMIs within 30–40% of monthly income.

4. Incomplete or Improper Documentation

Many loan applications get rejected simply because of improper or incomplete documentation.

Banks require clear and verified documents such as:

- Identity and address proof

- Income proof

- Bank statements

- Income tax returns

- Property documents (for secured loans)

Any mismatch, missing document, or unclear financial record can delay or even result in rejection.

5. Poor Presentation of the Loan Proposal

This is an underrated but very important factor.

Many borrowers actually qualify for loans but fail to present their financial profile properly. A poorly structured application can make the borrower appear riskier than they actually are.

Proper presentation includes:

- Clear financial information

- Organized documentation

- Proper explanation of loan purpose

Sometimes presentation makes the difference between approval and rejection.

6. Poor Financial Discipline

Banks carefully analyze the borrower’s financial behavior through bank statements and credit reports.

Indicators of poor financial discipline include:

- Frequent cheque bounces

- Irregular account activity

- Delayed EMI payments

- Excessive credit card usage

Such patterns raise concerns about repayment reliability and may lead to rejection.

7. Unclear or Risky Purpose of the Loan

Banks prefer lending for clear, productive, and justifiable purposes.

If the loan purpose is vague, speculative, or appears risky, lenders may hesitate to approve the application.

A well-defined purpose increases the bank’s confidence in the borrower.

Final Thoughts

Loan approval is not just about eligibility — it is about credibility, financial discipline, and proper documentation.

Borrowers who understand how banks evaluate loan applications can significantly improve their chances of approval.

Before applying for a loan, it is always wise to review your financial profile, maintain a healthy credit score, and prepare your documentation properly.

A little preparation can make a big difference.

✍️ At Arthvera, we aim to simplify banking and finance by sharing practical insights drawn from real banking experience.